ChatGPT

When Profitable Deals Get Stuck in the Pipeline

There's an unwritten rule in international business: goods must turn into cash faster than cash turns into new goods. When your capital rotation cycle stretches, the business starts gasping for air.

A profitable deal with a 30-day payment deferral can easily turn into a loss when you're forced to take out a payroll loan just to keep things running. Let's walk through a typical export transaction and see exactly where the money leaks.

The Anatomy of an Export Deal

Document Collection: The Paperwork Marathon

Export means paperwork. Mountains of it. Contracts, invoices, packing lists, certificates of origin (СТ-1 or Form A), phytosanitary certificates, export declarations. All this kicks off right after signing the contract, well before any shipment happens.

Where time bleeds out:

Waiting for certificates eats 3 to 7 days. Getting that certificate of origin often takes days, especially if you're missing an electronic signature or the inspector spots an HS code mismatch.

Translations and apostilles swallow another 2 to 5 days. If your counterparty demands notarized translations or legalized documents, add a minimum of two days right there.

Then there's the human factor, good for 1 to 3 days. Your manager suddenly remembers that shipping to Uzbekistan requires an invoice with net weight specified in a very particular format. Sound familiar?

Total time lost: 5 to 15 days before shipment even starts.

The real cost: Your bill of lading date shifts. Working under a letter of credit? A delayed shipment means amending that letter of credit — a paid bank service — or risk shipping late and triggering penalties.

Counterparty Checks and Currency Control

Even after your buyer has wired the money, banks have the right to freeze it for verification.

Where time bleeds out:

Sanctions screening runs 1 to 3 days. Banks scan to ensure your buyer or their bank isn't on any restricted lists. One mention of a yellow-flagged country and your payment slides into manual verification hell.

Document requests take another 2 to 4 days. For transactions above roughly 600,000 rubles, banks demand the contract. You provide scans, but they still need to physically "verify" them in their accounting systems.

A single digit wrong in the SWIFT code of an intermediary bank costs 3 to 7 days. The payment vanishes into the void and slowly makes its way back to sender.

Total time lost: 3 to 10 days after funds actually hit the country.

The real cost: Money sits on the bank's correspondent account, but not on yours. You can't pay customs for your next shipment. The goods wait. The clock ticks.

Financing Terms Negotiation

When you need a loan or factoring, the bank's internal machinery grinds into action.

Where time bleeds out:

Limit committees deliberate for 2 to 5 days. Even with an existing credit line, each new deal might need fresh approval if it exceeds previously agreed limits for that debtor.

Missing document requests add 1 to 3 days. The bank's lawyer wants your counterparty's charter with a certified translation. You wait a week for them to send an updated extract.

Total time lost: 3 to 8 days.

The real cost: You can't ship because there's nothing to pay the carrier. Finished goods pile up in your warehouse.

Confirming Performance

Banks and factoring companies need proof you actually shipped real goods, not just faxed fictional invoices.

Where time bleeds out:

Postal transit chews up 3 to 10 days. Under letters of credit, original bills of lading travel by physical mail from port to exporter's bank to importer's bank. In the 21st century.

Register verification drags for 2 to 4 days. For factoring, banks check whether the buyer actually signed the delivery notes. A smudged stamp on a document from Belarus? Reason enough to withhold payment.

Total time lost: 5 to 14 days.

The real cost: Money that should have arrived yesterday shows up in two weeks. You're begging suppliers for deferrals, losing early payment discounts, or grabbing expensive overdrafts. Margins shrink.

Final Payment

Everything's confirmed. Money's transferred. Home free, right? Not quite.

Where time bleeds out:

Exit currency control takes 1 to 2 days when repatriating export revenue or receiving loans in foreign currency.

Payment processing swallows 1 to 4 days. A payment sent Friday afternoon from Europe sits idle until Monday, landing Tuesday thanks to SWIFT and local clearinghouse schedules.

Technical overnights cost another 1 to 2 days. Funds hit the bank at 4:30 PM? They post the next business day. Period.

Total time lost: 1 to 5 days.

The real cost: Pure cash gap. You see the money, you can almost touch it, but you can't use it.

The Price of Delay: Putting Numbers on the Pain

Let's translate those days into hard numbers with a simple example.

Deal value: $100,000

Margin: 20% ($20,000 profit)

Average total delay across five stages: 20 days

Here's what actually happens:

Your cash gap widens. Salaries and rent don't wait. If your own funds are tapped out, the bank steps in.

That emergency money costs you. Average overdraft rates for working capital hover around 18% annually.

Borrowing $100,000 for 20 days costs: ($100,000 × 18% ÷ 365) × 20 = $986.

You're handing the bank nearly a thousand dollars just because your money arrived three weeks late.

Then your next shipment stalls. Customs goes unpaid. That second contract's potential profit — another $20,000 — evaporates.

And if your delay idles a vessel because freight charges weren't paid, prepare for penalties of $2,000 to $5,000 per day from the carrier.

Final tally: That $20,000 profit can shrink to $10,000 or $12,000 net, purely from timing losses in the financing chain.

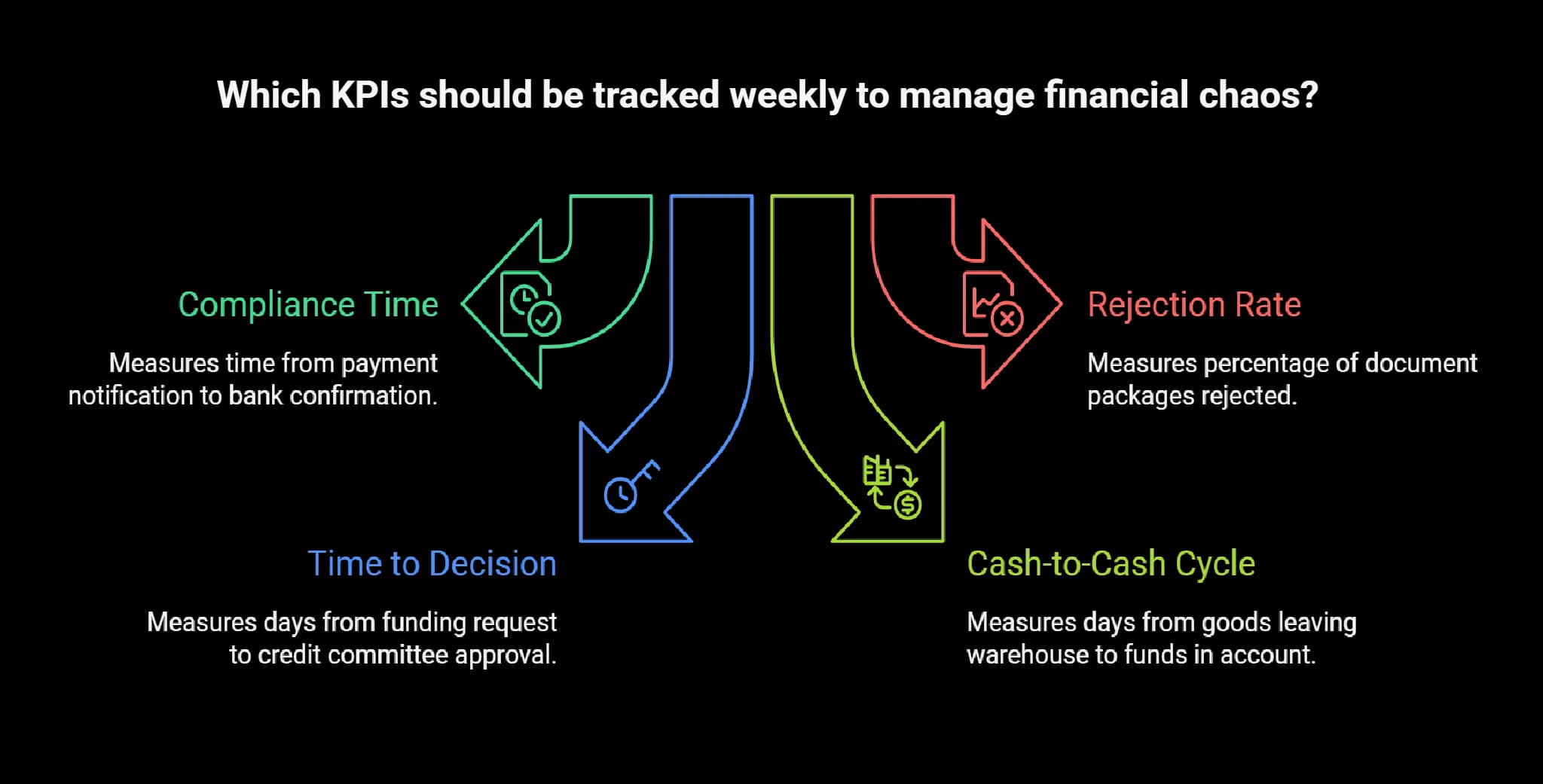

Four KPIs to Watch Weekly

Managing this chaos requires more than yelling at your bank. You need metrics. Here are four numbers every financial director or business owner should track weekly:

1. Compliance Time

What it measures: Time from payment notification or letter of credit application to bank confirmation that documents are accepted.

Target: No more than 2 business days.

Red flag: Consistently longer? Switch banks or push for fully electronic document exchange so they stop waiting for couriers.

2. Rejection Rate

What it measures: Percentage of document packages rejected by bank or buyer for errors.

Formula: (Number of returns ÷ Total transactions) × 100%

Target: Under 5%. If one in three packages bounces, your export department has a systemic problem.

Cost of failure: Each rejection costs at least 3 days.

3. Time to Decision

What it measures: Days from funding request to actual credit committee approval.

Target: 3 to 5 days for standard deals.

Trend warning: If this stretches, your bank's overloaded or your buyer's financial health is deteriorating.

4. Cash-to-Cash Cycle

What it measures: Days from goods leaving your warehouse to funds landing in your spendable account.

Target: Industry dependent. FMCG: 15 days. Machinery: 45 days.

Control signal: When last month's 25 days become this month's 40, you know exactly which of the five stages above to investigate.

Napkin.ai

Export financing isn't a sprint. It's an obstacle course relay. The winner isn't the company with the fattest margins — it's the one with the shortest money cycle. Track these five stages and four KPIs, and you'll finally see exactly where your company bleeds time and burns profit.