ChatGPT

How an Investor Enters a Deal: 7 Must‑Have Metrics

Ready to transfer money? Check the deal against 7 points. Learn which "red flags" guarantee capital loss and why perfect terms are a trap.

Investing is always about knowing how to ask the right questions before the money is transferred, and about cold calculation where others see only a "unique opportunity." Experienced investors know: a brilliant presentation and a charismatic founder are just packaging. The content is hidden in the numbers, documents, and legal nuances.

In this article, we will break down how to select deals. You will get a checklist of 7 must‑have metrics with specific entry thresholds, learn to classify risks by source, and find out which documents to study first.

7 Must‑Have Metrics for Entering a Deal

To quickly assess the attractiveness and risks of an investment proposal, use a "traffic light" system. It helps to visually split the deal's parameters into three categories: promising (green), requiring caution (yellow), and dangerous (red).

Here are 7 key metrics to pay attention to.

1. Investment Term

Green zone (enter): the term matches your investment horizon (e.g., 3–5 years). There is a clear schedule of key project milestones.

Yellow zone (check): the term is too short (less than a year) for this type of project, or, conversely, "perpetual" investments are offered with no clear exit mechanisms (triggers).

Red zone (ignore): the term is undefined. There is pressure to decide urgently, based on the principle "buy now, tomorrow will be too late."

2. Minimum Entry Amount (Equity Stake)

Green zone (enter): the amount is no more than 5–10% of your total capital, allowing you to maintain diversification principles.

Yellow zone (check): the investment requires 15–20% of your capital, creating a high concentration of risk.

Red zone (ignore): the amount exceeds 20% of your capital, or it is money you are not prepared to lose entirely. A particular risk is using borrowed funds to enter the deal.

3. Project Stage

Green zone (enter): Pre-IPO stage, a mature and stable business with a track record, production expansion projects.

Yellow zone (check): seed stage, especially if the product is not yet ready and exists only as a prototype.

Red zone (ignore): an "idea on a napkin." The project exists only as a presentation, with no real assets and no working product.

4. Collateral and Coverage

Green zone (enter): presence of liquid collateral (real estate, securities), a bank guarantee, or a guarantee from a large company. The ownership structure is transparent and clear.

Yellow zone (check): fixed assets or specific equipment (illiquid collateral) are offered as collateral, which would be difficult to sell.

Red zone (ignore): there is no collateral at all. Or "future periods" are offered as collateral. Assets are held in offshore structures with opaque and convoluted ownership.

5. Counterparty Type

Green zone (enter): a public company or a verified partner with a track record. In private deals, a partner from familiar jurisdictions (Russia, EU, UK) with understandable corporate governance rules.

Yellow zone (check): a new partner in the market, but with a "clean" check against the Unified State Register of Legal Entities (USRLE). Or an individual entrepreneur without extensive experience.

Red zone (ignore): a fly‑by‑night company (registered less than a year ago), a mass registration address, a nominee director.

6. Payment Schedule (Yield)

Green zone (enter): regular payments (coupon, dividends) from net profit. A transparent and clear calculation scheme.

Yellow zone (check): payments only at the end of the term, interest capitalization. Or a complex, confusing profit calculation structure that is hard to understand.

Red zone (ignore): a promise of "guaranteed" or abnormally high returns (2–3 times higher than the market). This is a clear sign of a financial pyramid (Ponzi scheme).

7. Exit Conditions

Green zone (enter): the exit mechanism is clearly stated in the contract: a put option, stock exchange listing, sale of the stake to a strategic investor. The asset's liquidity is clear.

Yellow zone (check): exit is possible only upon the occurrence of a certain event (IPO, business sale), but this is not backed by specific obligations and is more of a hope.

Red zone (ignore): exit conditions are absent from the contract. It is implied that you will have to find a new investor to sell your stake yourself.

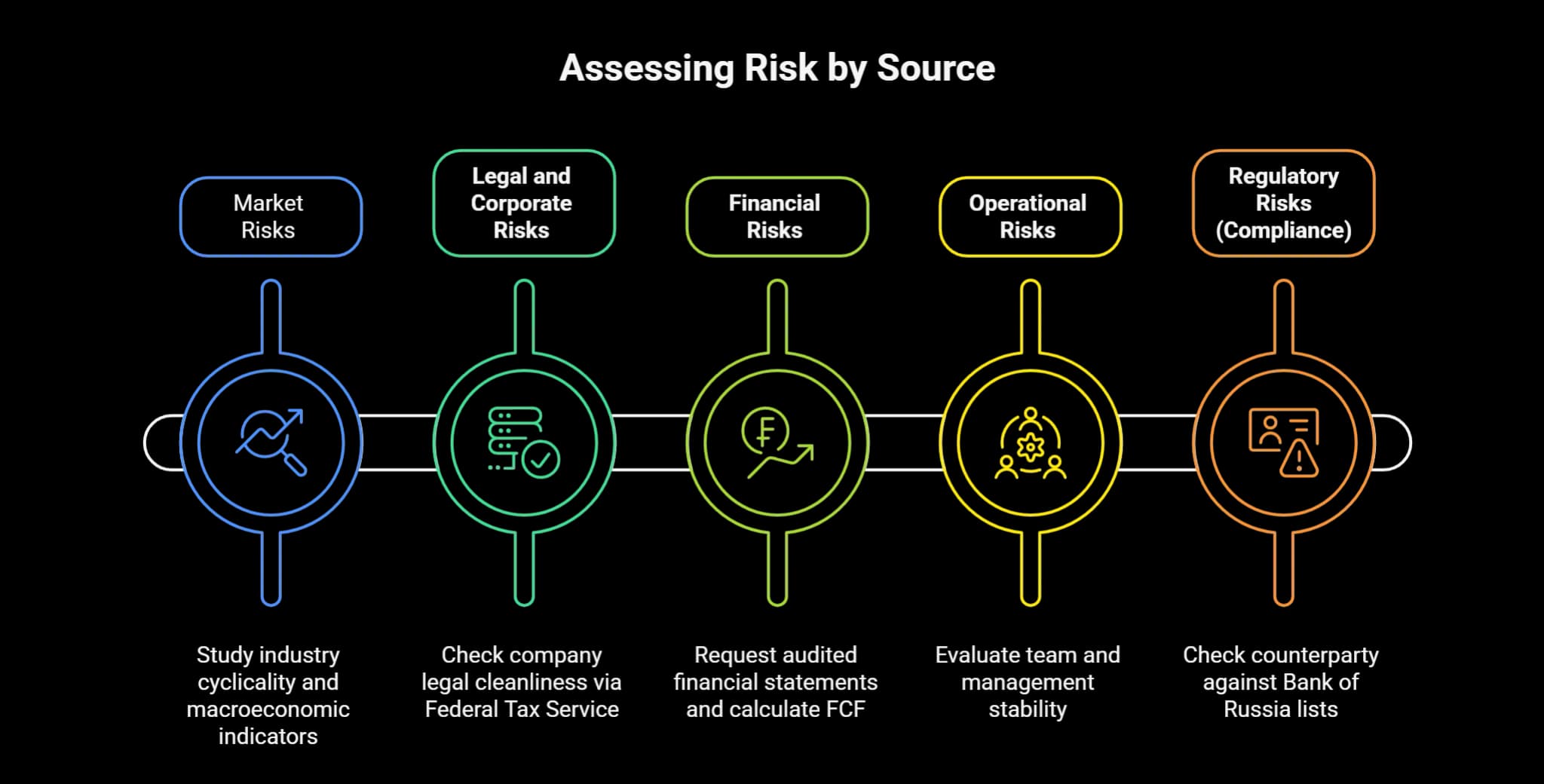

How to Assess Risk by Source

Risk is not an abstract concept, but quite concrete factors that can and should be assessed. Let's divide them into five sources.

1. Market Risks

These are related to the external environment. What happens if the market falls? If commodity prices collapse? If new technologies emerge that make the product obsolete?

How to assess: study the industry's cyclicality. Analyze macroeconomic indicators.

2. Legal and Corporate Risks

The risk that agreements will not be fulfilled or will be contested.

How to assess: check the company's legal cleanliness via the Federal Tax Service website (USRLE). Make sure there are no signs that the information is unreliable, and that the address and type of activity (OKVED codes) correspond to reality.

3. Financial Risks

The risk of not receiving profit or not recovering the principal amount of the loan.

How to assess: request audited financial statements for the last 3 years (if the project is mature). Calculate the free cash flow (FCF). If it is negative, the company is spending more than it earns — a reason to think twice.

4. Operational Risks

Internal company problems: departure of a key employee, equipment breakdown, missed deadlines.

How to assess: evaluate the team. How often does management change? Who is the key person? If everything hinges on one charismatic founder, that is a risk.

5. Regulatory Risks (Compliance)

Risks associated with government actions or sanctions.

How to assess: check the counterparty against the Bank of Russia website's lists for the "red zone" (high risk). Clarify whether the company is subject to sanctions restrictions.

Napkin.ai

Which Documents to Read First

Forget the beautiful brochure. Pick up the following documents — this is where the truth is hidden.

1. Information Memorandum

This is the base. Unlike a marketing presentation, the memorandum contains objective data: ownership structure, market analysis, reports, and a list of risks. Attention: if you are only given a presentation (a 10‑slide PDF) but they refuse to provide a memorandum, that is a red flag.

2. Term Sheet

A document that records the initial agreements. It may not be legally binding (except for confidentiality clauses), but it is the moral skeleton of the deal. It must clearly state the amount, the stake, the company valuation, exit conditions, and investor protection rights.

3. Shareholders' Agreement

The most important document after the main loan/share purchase agreement. It governs company management: how we vote, who hires the director, which decisions are made unanimously (veto rights). This is where the mechanisms for resolving deadlock situations are spelled out.

4. Due Diligence Report

If the deal involves serious money, this must be conducted by independent lawyers. They will verify the chain of title, the approval of major transactions, the legitimacy of share issuances, and director appointments. The absence of such a report or the presence of duplicated documents is a signal that the corporate history is messy.

Red Flags: Signals for Immediate Deal Rejection

Even if all the numbers in the table add up, there are things that cannot be ignored.

1. Too Good to Be True

You are promised returns significantly above the market with guaranteed capital preservation. This is a classic sign of either outright fraud or a risky asset whose risks are being hidden from you.

2. Pressure and Haste

Phrases like: "Invest today, tomorrow the slots are gone," "We have a closed round, I got you a 24‑hour slot." If the counterparty is rushing you, it means they are afraid you will have time to find the skeletons in the closet.

3. Opaque Structure

You do not understand where exactly the money is going. "A complex but very profitable scheme" is a marker that they are trying to confuse you.

4. Registration Problems

The company was registered a week ago. Or the legal address is listed in the Federal Tax Service database as unreliable. A deal with such a counterparty immediately puts you in the extreme risk zone.

5. No Crisis Plan

In response to your question "What will you do if sales drop by 50%?" you get sincere surprise and answers like "That can't happen to us." Experience shows: if an investor or founder brushes off risk discussions, they will abandon the project at the first sign of trouble.

Entering a deal for an investor is not gambling, but cold calculation. Remember: your main task is not to earn a "billion here and now," but to preserve capital so you can earn it in the future on quality assets. Be attentive, ask uncomfortable questions, and do not be afraid to walk away from negotiations if you see a red flag.